📅 June 15 is fast approaching. Have you paid your first Advance Tax installment?

A common misconception among taxpayers is that "Advance Tax" is a burden exclusively for large businesses and corporations. In reality, the Income Tax Department's rules are much broader. It applies to professionals, freelancers, consultants, traders, and even salaried individuals who earn significant income from other sources.

If you are earning income in India, ignoring Advance Tax can lead to heavy interest penalties under the Income-tax Act. Let’s break down everything you need to know to stay compliant and financially secure.

What is Advance Tax?

As the name suggests, Advance Tax is the income tax that you pay in advance, instead of a lump sum payment at the end of the financial year. Also known as the "pay-as-you-earn" scheme, these payments have to be made in instalments as per due dates prescribed by the income tax department.

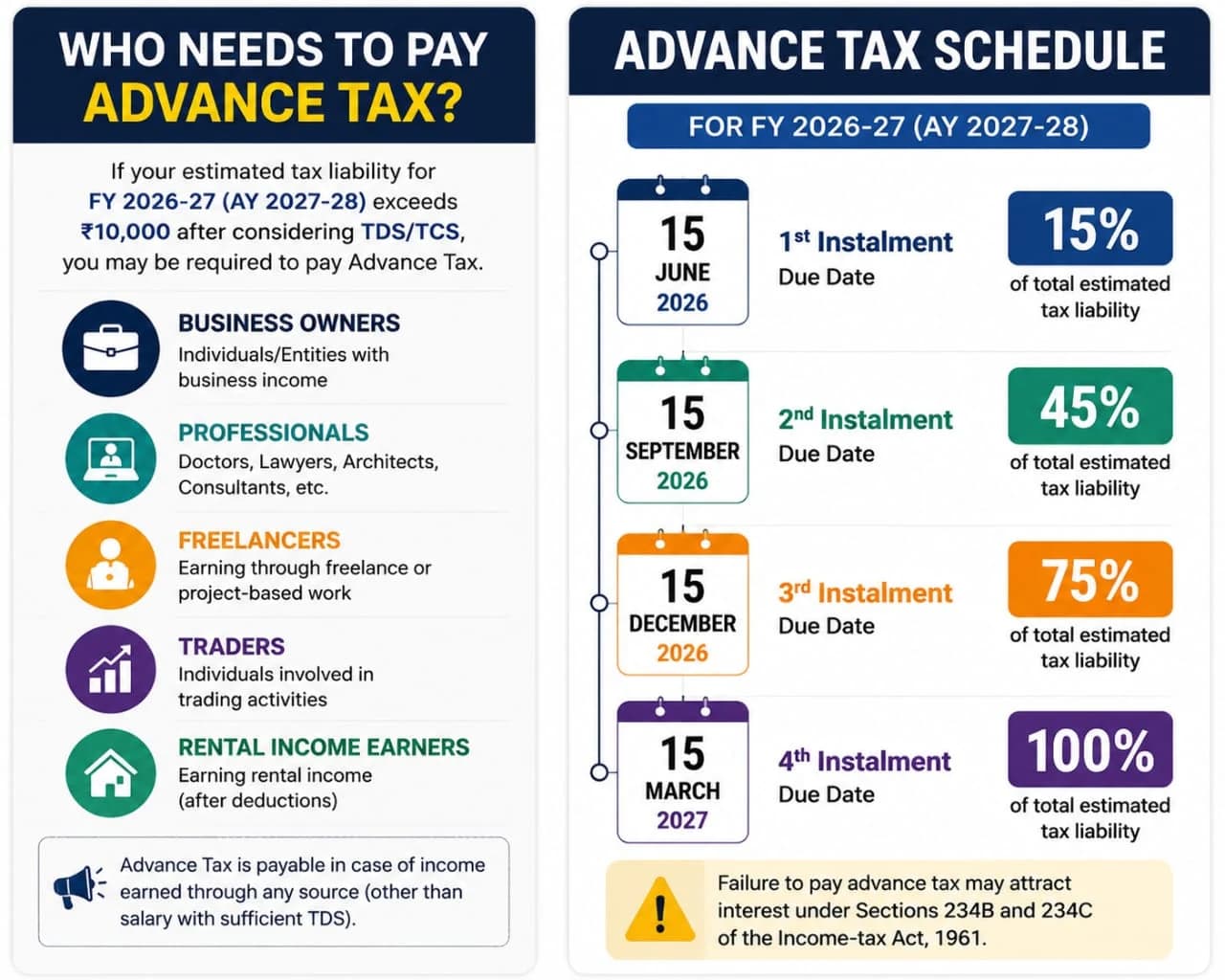

Who Needs to Pay Advance Tax?

The golden rule is simple:

💡 If your estimated total tax liability for the financial year exceeds ₹10,000 (after deducting TDS/TCS), you are required to pay Advance Tax.

This rule applies universally across various categories of taxpayers:

Professionals & Freelancers: Doctors, lawyers, architects, software developers, and freelance consultants.

Business Owners & Traders: Sole proprietors, partnerships, and companies.

Investors: Individuals earning significant income from capital gains (stocks, mutual funds, real estate), interest, or rent.

Salaried Individuals: If you receive a salary but also have high income from house property, capital gains, or other sources where TDS is not sufficiently deducted, you must pay Advance Tax on that additional income.

(Note: Senior citizens aged 60 or above who do not have any income from a business or profession are exempt from paying Advance Tax.)

Advance Tax Due Dates: Mark Your Calendar!

The Income Tax Department has divided the payment into four manageable instalments for most taxpayers (businesses opting for the presumptive taxation scheme under section 44AD/44ADA have different rules).

Here is the schedule you need to follow:

✅ On or before 15th June: 15% of the estimated tax liability

✅ On or before 15th September: 45% of the estimated tax liability

✅ On or before 15th December: 75% of the estimated tax liability

✅ On or before 15th March: 100% of the estimated tax liability

The Cost of Ignoring Advance Tax

Missing these deadlines or short-paying your advance tax isn't just a minor oversight; it comes with financial consequences. The Income Tax Department levies penal interest under:

Section 234C: Interest at 1% per month for the delay in payment or short payment of individual instalments.

Section 234B: Interest at 1% per month if you fail to pay advance tax or if the advance tax paid is less than 90% of the assessed tax, calculated from April 1st of the assessment year.

A Little Planning Today Saves Unnecessary Costs Tomorrow

Calculating your estimated income for the entire year in June can seem daunting, especially with fluctuating incomes from businesses or freelancing. However, proactive tax planning is crucial. By estimating your income, claiming your eligible deductions under Chapter VI-A (like Section 80C, 80D), and accounting for TDS, you can calculate an accurate advance tax figure and avoid giving away your hard-earned money as interest penalties.

Need Help Estimating Your Tax Liability?

Navigating tax estimations and ensuring timely compliance can be complex. You don't have to do it alone.

Reach out to the tax professionals at PK Lakhani before the due date. We can help you accurately project your income, maximize your deductions, and ensure your advance tax instalments are paid correctly and on time.

Contact us today to schedule a consultation and take control of your tax planning!